Volume Risk

By Garth Renne and Ken Truesdell in Energy Politics Archives Spring 2008

in the latest edition of our working history series, Garth Renne and Ken Truesdell remind us of the unanticipated risks of the Energy Transition offering some helpful hints at mitigation and risk management. Managing volumetric risk presents many challenges, not least of which is the fact that miss-steps can damage a company’s reputation, calling into question its understanding of its operations. With the continuing growth of alternative energy sources such as wind, and the expanding use of weather derivatives, expect volume risk to attract increasing attention in the next several years. The article, written in 2008 uses Brookfield Renewable Power and the volume risk challenges presented by its large and growing stable of hydroelectric assets in Canada.

Energy companies today have access to a suite of well-established tools and techniques to manage price risk, both in the context of proprietary trading as well as for asset management. The remaining debates in that area mostly concern what might be characterized as narrow technical details: the appropriate stochastic processes to model particular market prices, the best way to deal with uncertain and unstable correlations between products, and so on. In contrast, alternatives for assessing and managing volume risk remain less well developed, presenting risk managers with challenges when designing measures, limit frameworks, and reports, but also offering opportunities for creative work and unique, company-specific solutions. Brookfield Renewable Power Inc. (BRPI), a merchant generator, has grappled over the last several years with this issue as its portfolio has grown grown to approximately 3900 MW of primarily hydroelectric assets. 12

Apart from its relative infancy, there is a second, and perhaps more fundamental reason why volume risk management is of interest: executed poorly, it can be a greater threat to a company’s reputation than its price risk counterpart. Many companies have been criticized (often unfairly) for hedging programs that were perceived as ill-timed from a price standpoint. However, companies that misjudge their volume exposure, possibly leading to unexpected losses on ‘hedges’ not backed by production, can face far harsher investor reactions.

Questions can arise as to whether the company is properly maintaining its assets, or worse, doesn’t have a firm understanding of its operations. This article presents some key considerations in assessing volume risk, along with some suggestions for developing limit structures and managing uncertain production volumes. Although the perspective is one of a merchant hydroelectric generator, most of the observations also apply to other common cases of volume risk in the energy industry.

Volume Risk: Some Basic Considerations

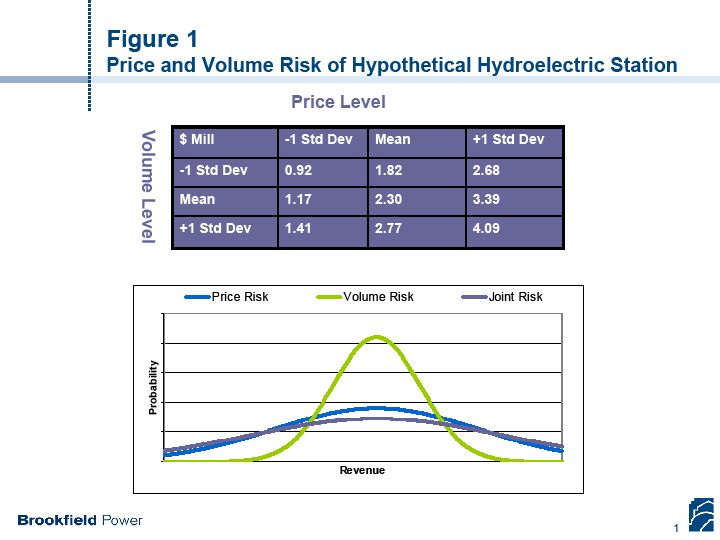

A very simple framework can illustrate some of the basic challenges of volume risk. Figure 1 shows a revenue profile from a single hypothetical -- but realistic -- plant on one of BRPI’s river systems.13 Clearly, the combination of volume and price uncertainty is a potent mix, with the multiplicative effect generating a huge potential range of outcomes. In practice, this can be compounded by the fact that in many regions, precipitation is concentrated in particular seasons – or even in a few discrete storm systems -- meaning that the range of volume uncertainty can behave more erratically than its price counterpart. The width of earnings at risk bands for hydro generating units often surprises risk oversight committees, but a few years of experience usually demonstrates how dramatic the combined effects of volume and price uncertainty can be.

Conclusions

It is certainly a time of inventiveness and innovation in the field of volume risk management, with room for companies to develop their own risk control frameworks and strategies. Weather derivatives and other structures are increasingly available as tools for companies seeking to lay off risks from uncertain production or loads. However, before embarking on a volume risk management program, particularly involving such tools, it is vital for a company’s middle office to have a solid bottom-up understanding of its volume and price risk distributions, including sources of correlations between those two dimensions.

Read full article here.

Notes

12 Brookfield Renewable Power Inc. (BRPI) owns approximately 3900 MW of generating capability, including 158 hydro plants, 2 gas-fired plants, a wind farm, and a share of a pumped storage facility. The vast majority of this capacity is located in Ontario, Quebec, New York, New England, and Brazil. BRPI is 100% owned by Brookfield Asset Management, which has over $US 70 billion of real estate, timberlands, and power plants under management.

13 The model is based on 25 years of actual daily precipitation and inflow data and a hypothetical run of river plant whose performance is related to inflows using historical relationships. Annual prices are distributed lognormally with a typical daily price shape. No systematic correlation between hydro output and prices is assumed in this model.